No products in the cart.

In a bad sign for airfreight, automotive logistics, charter volumes decline

Today, Road Runner Transportation Systems, a key player in the on-demand charter market, reported significant declines in financial performance, a symptom of the woes currently facing the automotive industry.

Road Runner (NYSE: RRTS) revenue dropped 14% and 13% year-to-date. Road Runner’s Active On-Demand segment revenues were down 26%. One third of this reduction — or about $13.4 million — was attributable to the General Motors strike, while the remainder was the result of declines in market volume and yield. The expectation is that the General Motors strike will lead to an overall $31 million hit in October compared to $17 million in September. GM is Road Runner’s largest customer.

After a bumper year in 2018 for automotive shipments by air and charters as shippers rushed to build inventory following a flurry of tariff announcements, 2019 has been a disappointment. Although Cargo Facts Consulting has not been able to identify any fundamental changes to the way manufacturers manage their logistics requirements, overall automotive inventories and inventory shipment ratios have been increasing. This is usually a bad sign for airfreight.

While overall assembly numbers are not down, car assemblies continue their decline as truck sales continue to become more dominant. And major manufacturers have been reporting declining production, plant closures and lower dealer inventories.

In the near term, Cargo Facts Consulting sees upside arising from the end of the GM strike, new model launches and factory retooling for electric vehicle production. However, the key driver for increased charter and airfreight activity will be inventory levels.

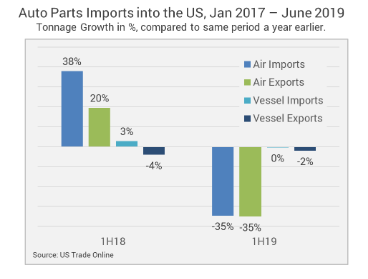

General Airfreight is down significantly but truck volumes are up

Airfreight imports and exports of car parts into and from the US were down by about 35% in the first half of 2019 compared to a year earlier and 10% compared to 2017. Airfreight transport suppliers in Mexico to the United States were down 40%. Yet vessel imports and exports have been holding up, with imports flat and exports down 2%. Trucking tonnage from Mexico to the US of cars and parts was up 10%.

On-Demand Charters are down too, but some carriers have found other opportunities

The Just-in-Time production model favoured across the auto industry leads to low inventory levels at assembly locations. When production levels are high and factories are operating three shifts a day, disruptions lead to the requirements for emergency charter and express shipments of parts and components to avoid interruptions in production. Automobile manufacturers generally do not budget for the requirement for so called “on-demand” services or include them as part of their service level agreements with their prime logistics providers. While the demand for such services is volatile by nature, the auto business as well as other industries such as oil and gas, healthcare, mining, high tech, telecommunications, among others, have created regular business opportunities for brokers and operators.

Demand for such services varies by auto manufacturer. Japanese manufacturers such as Honda and Toyota prefer to maintain their suppliers within several hundred miles of their assembly plants and, as a consequence, have less demand for on-demand charters. US manufacturers that source parts and components further afield and from Mexico are more likely to require emergency charters to recover from supply chain disruptions. Most of the auto related flying in the US takes place across between multiple cities across the Midwest from Mexico to Detroit. With the exception of Tesla’s California plant, this is where all of the US assembly plants are based.

However, in 2019, the two main go-to companies for automotive on-demand charters have both reported a decline in revenues and demand. Active on Demand, a division of Roadrunner Transportation systems reported a drop in expedited air fleet and brokerage revenues of 50% in the second and 29% in the third quarter of 2019 compared to a year earlier. This follows record growth of 16% in 2018, and 13% growth in 1st Quarter 2019. The results reported today indicate a continuation of this trend into the third quarter.

XPO also indicated that business held up well in January and February, but subsequently dropped. Expedited revenues are down more than 30%. Other charter operators interviewed as part of this analysis have also indicated a decline in charter requests and revenues. However, Cargobase, a freight trading platform, indicated that they had picked up a number of new automotive clients.

This drop in charter activity has had flow–on effect on carriers. The on-demand business sustains a diverse group of carriers operating small turboprop and jet aircraft. These include companies such as Aeronaves TSM, Alliance Air Charter, Amerijet, Berry Aviation, Everts Air, Freight Runners, Gulf and Caribbean Cargo, Sierra West, Kalitta Charters, Royal Air Freight and USA Jet Airlines. While the auto segment is down, carriers have found opportunity in other charter segments.

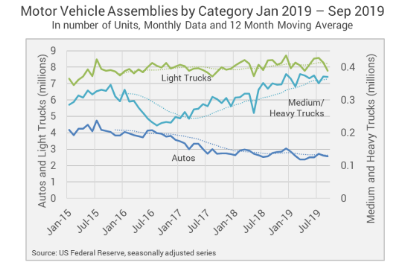

Motor Vehicle Assemblies remain flat, while inventories and inventory shipment ratios climb

Airfreight traffic and charters are down, motor vehicle assemblies in the US are not down in the first 9 months of 2019 compared to 2018, although they are about 8% below 2016/2017 levels. However, there are differences across segments. Consumers have been turning away from sedans and buying more light trucks and sports utility vehicles. This is reflected in assembly figures: sedans have been following a downward trend since mid-2016, while light trucks have been on a moderate upward trajectory.

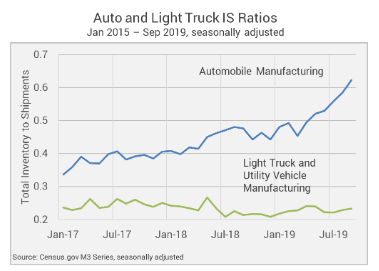

The key point for near–term air freight demand is that inventory to shipment ratios as well as inventories overall are up. Inventory to shipment ratios for automobile manufacturing are 31% higher compared to a year earlier. This is a killer for the requirement for airfreight and particularly emergency shipments of parts from suppliers to assembly locations. Light truck inventory to shipment ratios are up slightly by 9% compared to last year. Inventories overall are up 24% in the car manufacturing segment and 10% in the light truck segment.

Inventory–to–shipment ratios for the medium–to–heavy truck segment are 3% lower than last year. However, it is worth noting that this segment operates at much higher inventory levels than auto and light truck manufacturing.

There is upside in the near term

While overall car market demand is expected to be soft in the coming years, there could be some upside in the short–to–medium term for the air freight business and charter operators. Now that the GM strike has finished and production ramps up again, there could be additional requirements for charters to replenish inventory.

Moreover, many manufacturers — particularly Ford — are launching new models over the next 12 months which could lead to additional volumes as well. With many manufacturers retooling for electric and increased hybrid vehicle production, additional lift can be expected.

The key to watch, however, will be when inventories come down and inventory shipment ratios come back to normal levels.