No products in the cart.

Signs of post-Brexit turbulence ahead for U.K. airfreight

Shortly after the last votes were counted last Thursday, favoring the U.K.’s exit from the European Union by a margin of 52 percent to 48 percent, a slew of graphs appeared online parsing out the nuances of the complicated event. Examined in conjunction, the numbers uncovered some startling trends – most of them troubling for the now-independent island nation over the next few years.

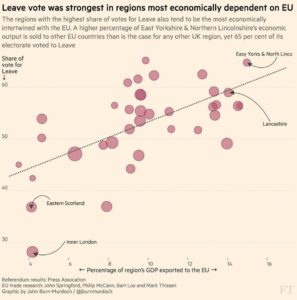

For instance, trade research by John Springford et al. (see graph below) based on referendum results from the Press Association showed voters in EU-trade-reliant areas were the most likely to vote in favor of leaving – a seemingly counterintuitive move. Regions such as East Yorkshire and North Lincolnshire voted overwhelmingly – both at 65 percent – for exit. These two regions have some of the highest E.U. trade figures, as a percentage of their economies. On the other end of the spectrum, Inner London and Eastern Scotland are among the lowest contenders for “share of economic output sold to other EU countries,” according to the aforementioned report. Interestingly, they also were overwhelmingly in favor of remaining in the union.

One headline in particular, S&P’s announcement that the U.K. could lose its AAA rating, underscores just how profound the economic implications are following the referendum. The news broke just hours after the final votes were tallied. The value of the pound against the dollar had already slumped to its lowest level in more than 31 years, down to $1.33.

An April report from the Organization for Economic Co-operation and Development (OECD), detailed the impact of lost trade across the English Channel under circumstances that are currently playing out. The report anticipated a “a major negative shock to the U.K. economy, with economic fallout in the rest of the OECD, particularly other European countries.”

In their most pessimistic scenario, the OECD researchers cautioned that “longer-term, structural impacts would take hold through the channels of capital, immigration and lower technical progress. In particular, labor productivity would be held back by a drop in foreign direct investment and a smaller pool of skills… By 2030, in a central scenario, GDP would be over 5 percent lower than otherwise – with the cost of Brexit equivalent to GBP3,200 per household [estimated before the GBP collapse this week].”

The OECD’s pessimism might be well placed. The Wall Street Journal reported on Friday that the pound traded down to $1.323 in early trading, the lowest level since 1985. The Economist reported that more than 10 percent of U.K. goods exports are shipped to Germany vs. approximately 7.5 percent the other direction. Overall, 51.4 percent of British goods exports are EU bound while only 6.6 percent of goods exports are headed in the other direction, the magazine said. These are the sort of exports, rather than services, that require complex infrastructure and equipment to move, involving jets, trains and trucks. The U.K. will have to scramble to make up that difference, and cannot expect a shoulder to cry on in Brussels.

Air cargo will face its share of the obstacles thrown up by new regulations likely to come online in the years ahead. According to Eurostat, in 2015 U.K. companies shipped 422,984 tonnes of airfreight to the EU, which represents a serious slice of total export values – with the EU accounting for more than half of total exports. The costs of shipping these goods will rise as integration breaks down and the U.K. leaves the union, which is cause for concern in the aviation business worldwide.