No products in the cart.

Airfreight traffic stagnates in dog days of August

As we head deeper into autumn and ever-closer toward peak season, the airfreight traffic numbers for August provided some pockets of good news, but offered little encouragement that the current air cargo stagnation has abated. According to reports from the International Air Transport Association (IATA), WorldACD and Drewry, August 2015 provided only the slimmest of indications of hope for better performance at the end of the year.

In IATA’s most recent airfreight market analysis, August saw weak overall air cargo traffic growth – just 0.2 percent, year-over-year – measured in freight tonne kilometers (FTKs). Regionally, the results swung from 10.4 percent growth, y-o-y, in the Middle East to a 7.3 percent, y-o-y, decline among Latin American carriers.

Looking at the year to date, IATA said worldwide air cargo traffic rose 2.6 percent in the first eight months, led by a 2.9 percent growth in international traffic and just 0.5 percent domestic growth. Most of the year-to-date growth recorded, IATA said, came in the first two months of the year, during the U.S. West Coast port crisis and the massive automobile recall. Minus those two events, underlying growth has been tepid for most of the year, IATA said.

The August results are better than July’s, where there was an overall 0.6 percent contraction in FTKs, but IATA cautioned that troubles still lie ahead in the ramp up to peak season. “All is not well,” IATA remarked. “Total volumes are down 2 percent compared to the end of 2014. And some of the key reasons for the earlier weakness – for example, downgraded growth expectations in emerging Asia, and the rebalancing the Chinese economy toward domestic consumption – are still there.”

WorldACD, meanwhile, echoed these concerns, saying that airfreight volumes for 2015 remain “stagnant” and that “yields keep falling.” Y-o-y air cargo volume for August, the organization said, increased by just 0.9 percent, while month-over-month yields, measured in U.S. dollars, fell yet again, this time by 1.2 percent.

Africa enjoyed a sizable volume increase in air exports of almost 10 percent, y-o-y, the WorldACD report said. The Latin America region posted positive yield numbers “for the first time in many months,” the report said, with month-to-month yields increasing by 3.5 percent for outgoing cargo and by 1 percent for incoming traffic. However, both Latin America and North America recording slightly negative volume growth, y-o-y.

“Falling yields ought to be good news for shippers and forwarders, yet they seem to take the view that – given the present low fuel cost – prices are not coming down fast enough,” the report said. The worldwide yield drop of 18 percent over the last 12 months “properly reflects lower fuel cost,” the report added.

To note changes in the market position of airlines, “grouped by where they come from,” WorldACD also compared air cargo volumes in the most recent 12-month period (September 2014 through August 2015) to those from the year 2012. Not surprisingly, carriers from the Middle East and South Asia had the largest increase, with volumes rising by 31 percent, compared to worldwide growth of 11 percent for the period.

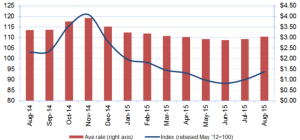

Also in August, Drewry’s East-West Air Freight Price Index indicated a price recovery of 3.7 points to an index of 93.7; this followed a 2-point recovery in July. “The index was lifted by strengthening rates on Asia origin trades into North America and Europe, despite notable declines in pricing on both legs of the trans-Atlantic,” said Simon Heaney, senior manager of supply chain research for Drewry. He said he expected to see airfreight pricing to strengthen through September and into October, “as new product launches boost short term demand.”